$200 Billion in Revenue: How an Aging Drug Will Conquer Pharma

An aging drug is a drug that has been rigorously shown to increase healthy lifespan in people, with emphasis on the ability of such an intervention to extend quality of life. It could allow older adults to enjoy a higher quality of life, for longer. The economics of delivering such value to human health at scale are unprecedented – we found that a drug approved and labeled for aging would conservatively have a peak global market size in the range of $150-$200 billion annually.

This size is ~4x the peak projected annual revenue of GLP-1s at $50 billion by 2030, ~6x the peak projected revenue of America’s soon-to-be best-selling drug, Keytruda (PD-1 cancer immunotherapy) at $30 billion annually by 2028, ~10x current bestseller Humira’s peak annual revenue (anti-TNF) at $21.2 billion in 2022, and ~15x the peak annual revenue of enormous blockbuster Lipitor (a statin) at $13 billion in 2013.

It’s also promising that the clinical trial to get this drug approved for aging and age-related disease on the label could potentially be as short as 3-6 years in length and cost $50-$100 million, within an order of magnitude of most Phase III clinical trials. Furthermore, just in the past month, we learned it was possible to get a drug approved and labeled for healthy lifespan extension in dogs by the FDA.

In this piece, we walk through an estimate of the market potential of an aging drug. We’ve also built an interactive model on Streamlit to allow anyone to play with key assumptions and numbers.

The aging drug TAM model

To build a model for the TAM of an aging drug, we need to answer:

3. What is the price of the drug?

4. What does adoption look like?

How large is the addressable market?

The total addressable market (TAM) for an aging drug refers to the entire potential customer base that could generate revenue for the drug, encompassing all individuals who might benefit from or be interested in using it. We based our foundational TAM size on the total number of adults aged 65 or older in the US from the 2017 US census data (see Appendix D for a table of values). This is a conservative estimate as it only reflects the initial target population. Over time this initial population may be expanded to those above 50 or 40 years old which would dramatically increase the peak market.

We also included non-US regions in this model. Given the US accounts for about half of global pharmaceutical sales, we approximated the inclusion of non-US populations by doubling the US revenue–avoiding the need for further estimation of population sizes and drug accessibility outside of the US. Also, we only included non-US populations for the reimbursement model, as regulations for DTC markets can vary drastically.

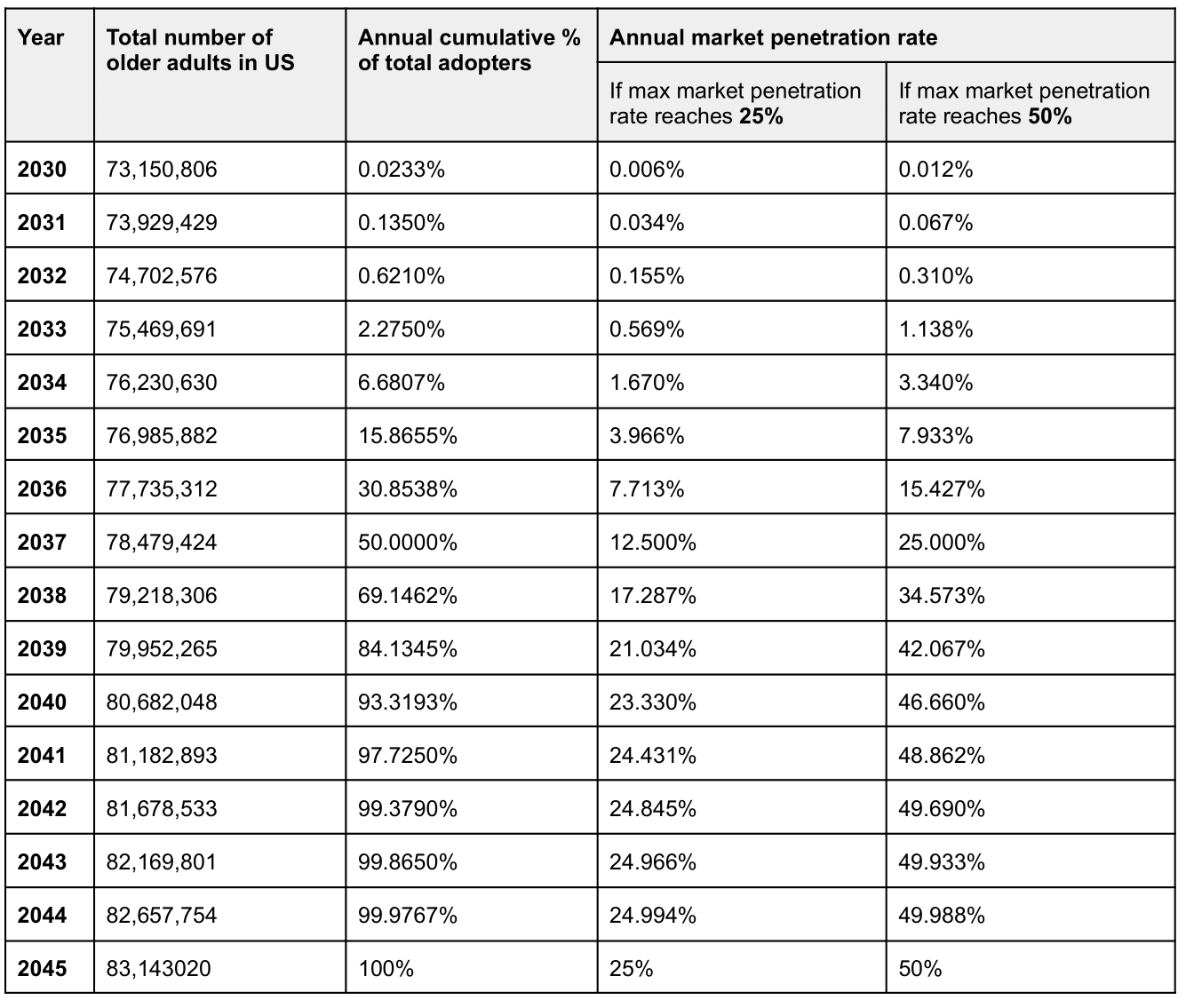

How big is the total addressable market in the US: Numbers range between 73 million people in 2030 to 83 million people in 2045 (see Appendix D).

Who will pay for an aging drug?

To know how much a drug is worth, we need to start with understanding who will pay for it. In the US, the majority of prescription medication costs are paid for by:

Commercial health insurers

Medicare Part D

Prescription drugs covered by insurance are far more accessible and frequently used by patients than those without coverage. Given that aging is closely linked with the increased prevalence of various diseases, typically managed with prescription drugs, a drug capable of effectively preventing these conditions could have significant implications. Such a drug would not only improve health outcomes by preventing the deterioration of the patient's health, but it would also reduce expenses for insurers by addressing the root cause rather than just treating symptoms.

Another path for an FDA-approved drug targeting aging could include the new direct-to-consumer (DTC) telemedicine approach in which users pay for services and medications out-of-pocket. By utilizing apps and online platforms, telemedicine companies give users access to convenient, on-demand care from licensed healthcare providers.

The rise of Hims, Hers, and Ro, three DTC telemedicine brands which started in reproductive health, exemplifies the potential of the approach in healthcare. By leveraging digital health, employing an effective consumer marketing strategy, and destigmatizing traditionally sensitive health topics, Him, Hers, and Ro have shifted the Overton window of how consumers access and perceive healthcare solutions. If a drug designed to slow down the aging process receives FDA approval, it could initially pursue a DTC route, especially before long-term health outcomes and economics research can show financial benefits for insurers and other payers.

To convey the potential scope of future market developments, the increasing interest in obesity drugs serves as an insightful example. This trend hints at the emergence of a pharmaceutical product with revenue potential comparable to the most lucrative products currently in the market. For instance, it's conceivable that drugs like GLP-1 could surpass even the iPhone in sales and profitability. This is particularly relevant when considering the willingness of the average American to invest $500 monthly for weight management. For a more in-depth analysis, the Stifel report, particularly the aging total addressable market (TAM) section on slide 126, offers a comprehensive overview of this market's potential.

Who will pay for it: 1) commercial health insurers and Medicare (reimbursement model) and potentially 2) DTC markets (cash-pay model)

What is the price of an aging drug?

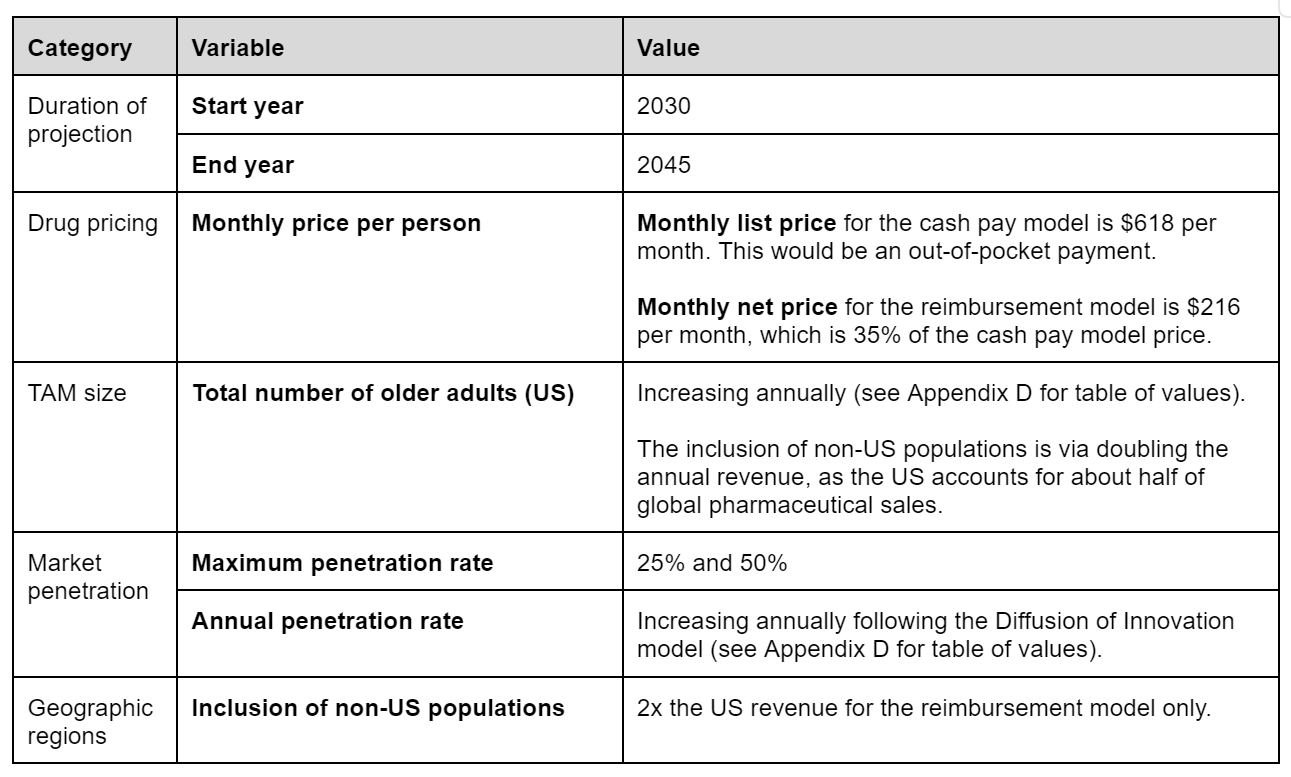

To predict the price of an aging drug, we estimated the monthly list price for a cash-pay model and the monthly net price for a reimbursement model.

The list price is what the manufacturer sets for a drug before negotiations or discounts, which might reflect DTC market prices. We estimated based on existing medications taken by older adults at scale, such as antidiabetics and cardiovascular drugs (Appendix D). The average out-of-pocket cost of the name-brand version of these drugs is set as the monthly list price, at $618 per month (Appendix C).

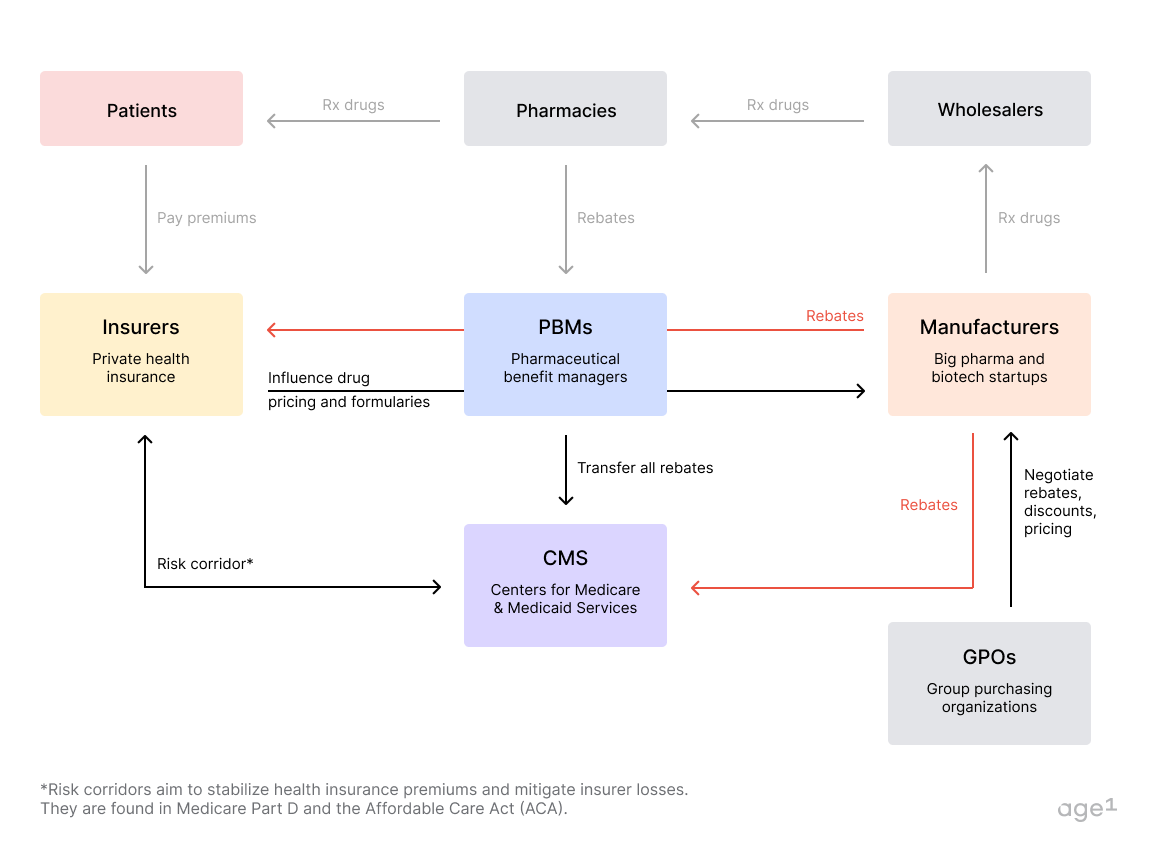

In reality, a consumer pays something closer to the net price after discounts and rebates, determined via negotiations between pharma industry stakeholders. In the US, this comprises patients, insurers, pharmaceutical benefit managers (PBMs), pharmacies, wholesalers, manufacturers, and government entities like the Center for Medicare & Medicaid Services (CMS). Figure 3 provides a summary of how US drug pricing works, with complementary details in Appendix C.

Following negotiations with PBMs, drug manufacturers usually absorb a portion of the drug costs. Currently, the reduction from the monthly list price ranges between 40-60%, with an average of around 50%. With shifting policies around drug rebates, this reduction might escalate to between 70% and 75%. Therefore, we considered an average reduction of 65% from the monthly list price for our calculations.

For the reimbursement model, the monthly net price would be $216, which is 35% of $618.

Estimate of the price of an aging drug: $216 per month (reimbursement model) or $618 per month (cash-pay model)

What does adoption over time look like?

For the maximum penetration rate (percentage of the TAM captured), we considered the following patient adherence numbers to approximate a range of 25% to 50%:

Half of all American adults get the flu vaccine every year.

Patient adherence to chronic medications is about 50%.

Patient adherence to cardiovascular medication (treatment dependent) ranges from 25-50%.

In one study: of 400,000 people eligible to take statins, about 20% were chronically taking them.

For the annual penetration rate, we applied the Diffusion of Innovation model to approximate a nonlinear increase in market capture as the adoption rate grows over time; detailed values and estimations for annual penetration rates are provided in Appendix D.

What is the adoption of an aging drug over time: Assuming a 25% penetration rate, the numbers range from 0.006% in 2030 to 25% in 2045. Assuming a 50% penetration rate the numbers range from 0.012% in 2030 to 50% in 2045.

Calculating the annual revenue of an aging drug

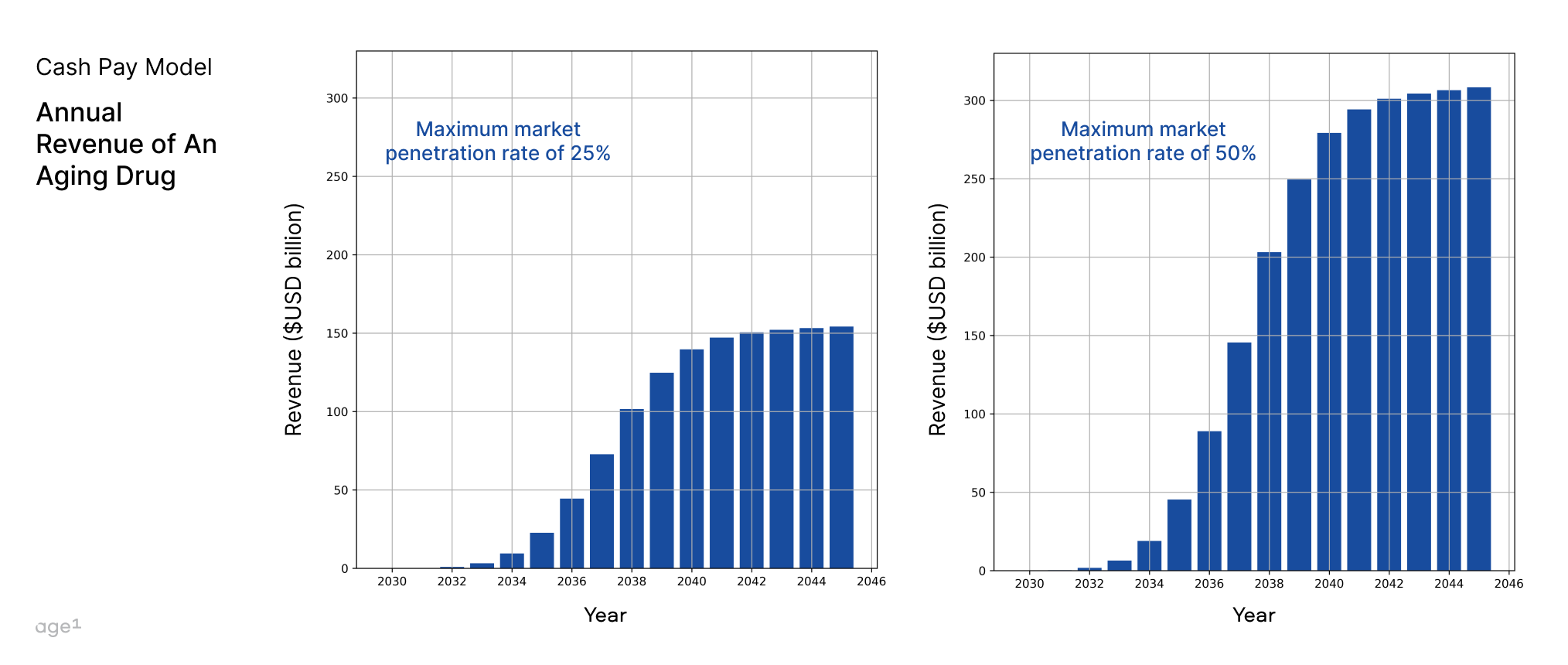

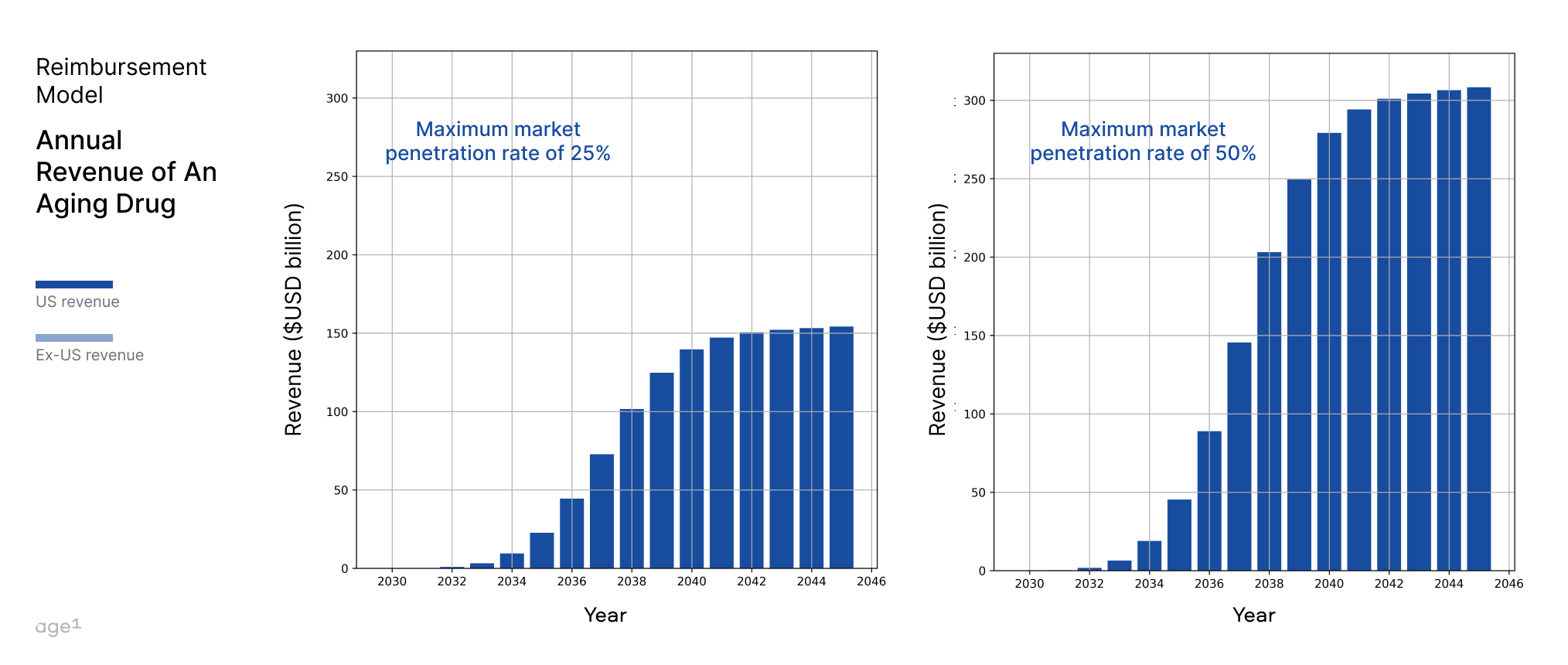

The duration of projection is from 2030 to 2045, with 2045 being the end year plus the duration of drug patent exclusivity. This period ranges from 10 to 20 years, so we took 15 years as an average. Table 1 summarizes the key assumptions and variables considered. Now, we can calculate annual revenue as

= total number of adults × annual penetration rate × monthly price/person × 12 months/year

Figures 5 and 6 show annual revenue for the cash pay model and reimbursement models, respectively, at 25% and 50% maximum market penetration rates.

Between the cash-pay and the reimbursement model, the reimbursement model will likely dominate–reduced prices mean greater accessibility and with proven efficacy, greater accessibility will enable broader adoption. So, we used a reimbursement model with a 50% maximum market penetration rate to compare against other blockbuster drugs in terms of peak or peak-projected revenue (Figure 1).

Conclusion

The approval of a drug targeting the aging process could lead to a seismic shift in healthcare. The potential long-term healthcare savings are vast, as was with statins, which significantly reduced expenditure for inpatient care from hospitalization (see Appendix E).

With the potential to yield conservatively up to $200 billion annually, a company that owned only this drug would be more valuable than the top two big pharma companies (J&J and Pfizer) in terms of revenue… combined. We believe that this drug has the potential to become the largest product in human history, even larger than the iPhone.

We fully acknowledge that this estimation exercise is simplified. One factor we didn’t account for is the impact of the Inflation Reduction Act (IRA) in the later revenue lifecycle (roughly 9 years into the patent exclusivity period for a small molecule, and 13 years for a biologic). While ongoing Medicare negotiations will likely lower the price of such drugs, this hopefully increases their accessibility to the general public. So, even with a reduced price, the overall market size could increase.

It’s crucial to underline that our discussions remain hypothetical; we're venturing into uncharted waters, grappling with vast numbers and concepts that few yet perceive. However, we hope that the concept of an aging drug with some quantifiable economic value moves the needle closer from the abstract to the tangible.

A key question remains–is it even possible to get a drug approved and labeled for aging and age-related diseases in humans? We’ll explore this topic in depth in a future piece.

Written by: Alex Kesin, Maggie Li, and Alex Colville.

Acknowledgements: Wen Kin Lim, Dr. Joan Mannick, Laura Deming, Lily Clayton, Ada Nguyen, Carol Magalhaes, and Raiany Romanni.

Further reading

The Secret Cambrian Bio Master Plan to Build Drugs to Treat Aging (just between you and me)

Medicare Coverage of Weight Loss Drugs Could Significantly Reduce Costs | USC Schaeffer

Inside the push to get weight loss treatment covered by Medicare | The Hill

Appendix A. List of drugs commonly taken by older adults

Antidiabetics (for type 2 diabetes)

GLP-1 receptor agonists (current approved versions listed here are not small molecules, but a must-have contender for age-related disease. Stay tuned to an upcoming piece for why they are important!)

SGLT2s

Biguanides

Metformin (Glucophage)

Cardiovascular health

Beta-blockers

Statins

Angiotensin-converting-enzyme (ACE) inhibitors

Bone health

Central nervous system

Appendix B. Price of brand name drugs commonly taken by older adults

Values for the out-of-pocket price per month are from GoodRx.

Appendix C. Breakdown of drug pricing and payer coverage in the US

In the U.S. pharmaceutical industry, a complex web of financial transactions connects patients, insurers, pharmaceutical benefit managers (PBMs), pharmacies, wholesalers, manufacturers, and government entities like the Center for Medicare & Medicaid Services (CMS). Figure 7 provides an overview with examples.

Patients fund insurers through premiums; insurers then pay for drugs and services to pharmacies and manufacturers, with CMS mediating financial activities for Medicare/Medicaid. Manufacturers grant rebates to PBMs and pharmacies, influencing drug pricing and insurance formularies, with a share of rebates going back to insurers. CMS's role in rebates, affected by legislation like the Inflation Reduction Act (IRA), and the involvement of Group Purchasing Organizations (GPOs) in price negotiations, further complexify the system. The entire process dictates medication pricing and accessibility, underlining the intricacy of healthcare economics. Here is a quick video that explains Rx drug rebates and premiums.

Coverage by payers for patients

The older adult population is split in terms of coverage by payers: among older adults (aged 65 and over), 40.9% were covered by private insurance (with or without Medicare), 28.0% had Medicare Advantage, 13.6% had traditional Medicare only, 8.9% had some other coverage (including military coverage without Medicare), 7.6% were covered by Medicare and Medicaid (dual-eligible), and 1.0% were uninsured. Of all Medicare recipients, around 74% are enrolled in Part D.

Appendix D. Growth of drug price, TAM size, and market adoption over time

The monthly list price and the monthly net price correspond to the drug pricing used for the cash-pay and reimbursement models, respectively.

The total number of older adults in the US are interpolated values from 2017 US census projections of total population size and percentage of the total population aged 65 and older until 2060.

The annual market penetration rate is found by multiplying the annual cumulative percentage of total adopters by the maximum market penetration rate. Following the Diffusion of Innovation model, the cumulative percentage of total adopters is found by approximating the area under the bell curve. Over time, as evidence of the drug's efficacy grows, more individuals will likely adopt it, with a non-linear growth trend similar to the red curve in Figure 2.

Appendix E. Learnings from statins for long-term Medicare savings

If massive long-term savings in terms of improved quality of life and reduced healthcare costs due to chronic conditions become clear, then the way Medicare spends on a drug approved and labeled for aging and negotiates pricing with drug manufacturers could look very different. This similarly applies to commercial health insurers. Insurers at the end of the day care about cost savings and value so it’s important to think about this part of an aging drug.

In our analysis, we presented a simplified model for projecting reimbursement model revenue based on cash-pay revenue. However, the actual situation is more complex, especially when considering Medicare. Medicare's reimbursement is contingent upon cost-effectiveness; they reimburse for treatments that demonstrate savings, meaning an aging drug must prove to be cost-efficient.

Here, we can learn from the story of statins.

Imagine you are a person aged 65+ with high LDL (bad cholesterol) in the early 1980s. Your doctor is concerned about your cholesterol level’s potential impact on your heart health; they recommend you improve your lifestyle. If there’s an exceptional concern, they might put you on a fibrate, a class of cholesterol-altering drugs.

A few years into the late 80s; the first statins have been approved and are now cautiously being prescribed to those who most need them. While it is known they are effective at lowering LDL cholesterol, they’re so new on the scene that you’re not likely to get your hands on one. If you were, you’d likely have to pay at the full list price: not only did Medicare Part D – the payer that would make statins affordable for patients–not even exist yet, but nobody knew what these things were! Good luck trying to get private insurance to cover a medication nobody had even heard about.

Fast forward to 1994. The 4S study–a multi-year trial of a statin called simvastatin – is completed and its findings published in the Lancet, and the results are stupefying.

The few thousand patients with a history of angina/heart attacks who were on a statin saw a ~35% reduction in LDL-C and a ~30% decrease in overall mortality. Perhaps most relevant of all: hospitalization costs went down 32% in the statin-taking group, demonstrating that statins were cost-effective in addition to significantly improving the quality of life in patients with coronary heart disease.

Essentially, payers would be saving money if they paid to get their patients on statins, as opposed to the status quo. Since then, statins have become some of the most commonly prescribed drugs in America. Lipitor has grossed $163 billion in sales since its release in 1997, making it the third-best-selling drug of all time. Backtesting savings for payers on simvastatin (a statin) in the 90s, the estimated price per patient via savings comes out relatively close to the actual price at the time for the drug.

According to this 1995 paper, the estimated expenditure for inpatient care (e.g. hospital care, nursing home care) was $8 billion. If you recall from the 4S paper, simvastatin reduced hospital costs by ~30%, so we could crudely estimate savings by the following formula:

$ savings = $ expenditures * % savings → $8 billion * 0.3 = $2.4 billion / year in savings

Divide the savings by the number of patients (~2.6 million hospitals admit patients with heart failure per year according to the paper) and we should get a reasonable number for the pricing of the brand name Simvastatin (Zocor).

Inflation-adjusted $2.4 billion from 1995 dollars to 2023 dollars is $4.84 billion

$4.84 billion savings / 2.6 million patients = ~$2017 in savings per patient every year

A yearly prescription of $3,718.96 per year is ~$168 per month for patients, cash pay.

In 1995, the wholesale list price for a 30-tablet supply of simvastatin (Zocor) was $54.00 for 20mg and $97.80 for 40mg. Adjusted for inflation, that would be $111.87 on the low end (20mg) and $202.61 on the high end (40mg). A price of $202.61 per month falls in the same ballpark as $168 per month.

The main takeaway from statins? The potential cost-effectiveness of an aging drug matters a lot: patient adoption depends on insurance coverage, which highly depends on the savings of said drug.

Using Medicare spending data to validate the reimbursement model

Based on Medicare spending data from 2018, we can complete a similar calculation. For starters, here is the spending data from that year per disease:

Notice that a lot of these diseases are comorbid–which is likely why the final total is quite big. Instead of opting for this number, we could instead refer to the number that Medicare quotes as their annual spending of $829 billion in 2021. That would put spending at $942 billion, adjusted for inflation.

Taking statins as an example, which decreased hospitalization expenses for heart disease by 30%–if an aging drug could achieve a similar reduction in the expenditure related to age-associated diseases for Medicare–it could result in savings of approximately 30% of $942 billion, equating to around $283 billion in savings annually.

When considering our reimbursement model, which estimates US. revenues of $50 to $100 billion annually from such a drug, it appears that the spending by Medicare could shift some spending from a range of drugs to an aging drug. Nevertheless, this would still result in a net saving of around $183 to $233 billion each year for Medicare.